Four years ago, my closest friend received a phone call on an otherwise unremarkable Tuesday morning that changed everything about his financial life in an instant. His employer of seven years informed him, along with a third of the company’s workforce, that his position had been eliminated effective immediately. He had two weeks of severance pay, a mortgage payment due in eighteen days, and exactly enough money in his bank account to cover groceries for the next ten days.

What followed was one of the most stressful periods of his life, not because losing a job is easy under any circumstances, but because the complete absence of any financial cushion transformed what should have been a difficult but manageable setback into a genuine crisis. He borrowed money from family members, fell behind on his mortgage, accumulated credit card debt at punishing interest rates trying to cover basic living expenses, and spent the following two years slowly and painfully digging himself out of a financial hole that a single, relatively straightforward financial preparation could have prevented entirely.

His story is not unusual. Research consistently shows that the majority of working adults in most countries would struggle significantly to cover an unexpected expense of even a modest size without borrowing money or selling assets. In a world where job losses, medical emergencies, car breakdowns, appliance failures, and unexpected home repairs are not rare catastrophic events but routine features of ordinary adult life, this widespread lack of financial preparation has consequences that are both financially devastating and psychologically crippling.

The solution is not complex, not sophisticated, and does not require a high income or advanced financial knowledge to implement. It is called an emergency fund, and in this guide, you will learn exactly what it is, precisely why every financial expert in the world agrees it is the single most important financial step you can take before anything else, and the specific, practical steps to build one starting from wherever you are financially right now.

Whether you are starting from zero, recovering from debt, earning an irregular income, or simply someone who has always meant to build an emergency fund but never quite gotten around to it, this guide will give you everything you need to finally make it happen.

What Is an Emergency Fund and What Does It Actually Cover?

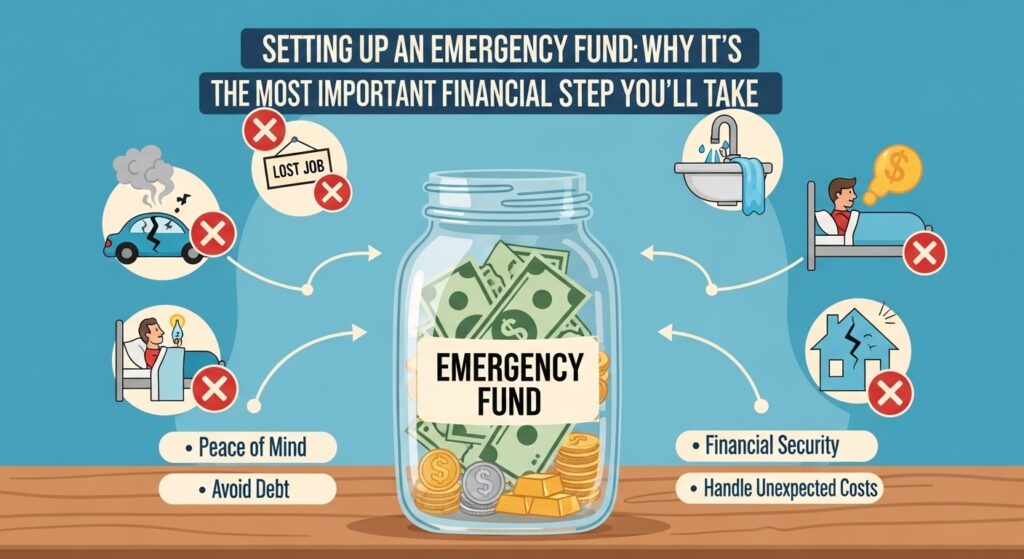

An emergency fund is a dedicated reserve of liquid cash, money held in an accessible savings account, set aside exclusively for genuine, unexpected financial emergencies that would otherwise force you to borrow money, sell assets, or fall behind on essential financial obligations.

The word “emergency” is doing important work in that definition, and understanding it clearly from the beginning will prevent one of the most common mistakes people make with emergency funds, treating them as a general savings buffer that can be dipped into whenever a financial inconvenience arises rather than a protected reserve for genuine crises.

What Qualifies as a Genuine Emergency

A genuine financial emergency is an unexpected, necessary expense that significantly threatens your financial stability or your basic standard of living and that you could not reasonably have anticipated and planned for in your regular monthly budget.

Qualifying emergencies typically include sudden job loss or a significant reduction in income, urgent medical or dental treatment not covered by insurance, essential car repairs needed to maintain your ability to work or fulfill critical responsibilities, critical home repairs such as a burst pipe, broken heating system, or structural damage, and emergency travel required to respond to a family crisis.

What Does Not Qualify as an Emergency

An equally important part of understanding your emergency fund is being honest about what does not qualify for withdrawal. A sale on something you have been wanting to buy is not an emergency. A vacation you did not budget for is not an emergency. A new phone because your current one is aging but still functional is not an emergency. Holiday gifts, home improvements, and planned large purchases are not emergencies, they are predictable expenses that belong in their own dedicated savings categories within your regular monthly budget.

This distinction matters because the psychological protection your emergency fund provides depends entirely on its integrity. An emergency fund that gets raided for non-emergencies provides neither the financial security nor the peace of mind that is its entire purpose. Protecting it with clear, honest rules about what constitutes an emergency is as important as building it in the first place.

Why Financial Experts Unanimously Agree This Comes Before Everything Else

If you have spent any time reading personal finance advice, you will have noticed a remarkable degree of consensus among financial advisors, economists, and money educators who disagree on virtually every other aspect of financial planning, about investment strategies, about debt repayment approaches, about retirement planning philosophies, about tax optimization techniques. On the subject of emergency funds, however, the agreement is essentially universal: build your emergency fund before you do anything else with surplus money.

Understanding why requires understanding what happens in its absence.

The Debt Trap That Emergency Fund Absence Creates

Without an emergency fund, every unexpected expense, no matter how modest relative to your income — becomes a potential debt-generating event. When the car breaks down and the repair costs more than you have available in your checking account, you reach for a credit card. When a medical bill arrives unexpectedly, you borrow. When a gap in employment leaves you short on rent, you turn to a personal loan or a family member.

Each of these individual responses to a single emergency feels manageable in isolation. The problem is that these events do not happen once, they happen repeatedly throughout a financial life, and each one that generates debt makes the next one more likely to generate additional debt, because a portion of every subsequent paycheck is now committed to servicing previous emergency debt rather than available to rebuild a financial reserve.

This is the debt spiral that an emergency fund specifically and directly prevents. When the car breaks down and you have an emergency fund, you pay the repair bill, feel the temporary sting of a reduced balance, and begin the straightforward process of rebuilding. When the same event happens without an emergency fund, you accumulate debt that costs you additional money in interest every single month until it is repaid, turning a one-time financial setback into a multi-year financial burden.

The Psychological Protection Is as Valuable as the Financial Protection

The financial case for an emergency fund is compelling enough on its own. But the psychological case is equally powerful and far less frequently discussed.

Living without an emergency fund creates a state of chronic financial anxiety — a persistent, low-level stress that affects decision-making, relationships, sleep quality, and general wellbeing in ways that are difficult to quantify but very real to experience. When you know that a single unexpected event could destabilize your entire financial situation, the awareness of that vulnerability sits in the background of daily life as a constant source of tension.

An adequately funded emergency fund eliminates that anxiety almost entirely. It transforms your relationship with financial uncertainty from fearful to genuinely confident, because you know, with concrete certainty, that if something goes wrong you have the resources to handle it without catastrophic consequences. That psychological shift, from financial fragility to financial resilience — is one of the most profoundly life-improving changes that a relatively modest amount of saved money can produce.

Step 1 — Determine Your Emergency Fund Target

Before you begin building your emergency fund, you need to know what you are building toward. The standard recommendation from most financial advisors is to accumulate between three and six months of essential living expenses — the amount required to maintain your basic standard of living, covering your needs category from the 50/30/20 framework, for that period without any income. (For a complete guide to calculating and managing your essential expenses, check out our article on [How to Create a Monthly Budget That Actually Works: The 50/30/20 Rule].)

Calculating Your Personal Emergency Fund Target

The first step is calculating your monthly essential expenses, the genuine needs that must be paid regardless of circumstances. This includes your rent or mortgage payment, essential utility bills, basic grocery costs, minimum debt payments, essential transportation costs, and critical insurance premiums. Add these up to arrive at your total monthly essential expense figure.

Multiply that monthly figure by three to establish your minimum emergency fund target, the amount that would carry you through three months without income. Multiply by six to establish your full emergency fund target, the more conservative and ultimately more protective figure that most financial advisors recommend as the standard goal.

How Much Is Right for Your Specific Situation?

The appropriate size of your emergency fund is not identical for every person, it depends on several factors specific to your circumstances. A person with a stable, salaried position in a secure industry, with no dependents and relatively low fixed monthly expenses, may be adequately protected by a three-month fund. A freelancer with variable income, a self-employed business owner, someone with dependents, a person in a volatile industry, or anyone with significant fixed monthly commitments should aim for the six-month target or potentially beyond.

When in doubt, err on the side of more rather than less. The cost of having a slightly larger emergency fund than you strictly needed is minimal, a modest amount of foregone investment returns on the excess cash. The cost of having a smaller emergency fund than you needed when a genuine crisis arrives is potentially catastrophic. The asymmetry of these outcomes makes the conservative approach the rational one.

Step 2 — Choose the Right Account for Your Emergency Fund

Where you keep your emergency fund is not a trivial decision. The account you choose must satisfy two requirements that exist in some tension with each other: it must keep your money genuinely accessible for immediate use when an emergency arises, and it must keep your money sufficiently separate from your everyday spending accounts to prevent casual erosion through non-emergency withdrawals.

Why Your Regular Checking Account Is the Wrong Choice

Keeping your emergency fund in the same checking account you use for daily spending is the most common emergency fund mistake, and it is one that undermines the fund’s effectiveness in two distinct ways.

First, money that is immediately visible and accessible alongside your regular spending balance becomes psychologically integrated with your general available funds — making it significantly harder to resist the temptation to spend it on non-emergencies. Second, the low or zero interest rates paid on most checking accounts mean your emergency fund earns virtually nothing while it sits there, missing the opportunity to at least keep partial pace with inflation.

The Ideal Emergency Fund Account

The ideal home for your emergency fund is a dedicated, separate high-yield savings account — one opened specifically and exclusively for your emergency fund, with a clear mental designation that the money in this account is not available for any purpose other than a genuine financial emergency.

High-yield savings accounts offered by online banks and digital financial institutions typically pay significantly higher interest rates than traditional branch-based savings accounts — in many cases four to five times the national average savings rate. While the interest earned on an emergency fund will not make you wealthy, choosing a high-yield account over a standard one means your emergency fund is working as hard as possible while waiting to be needed.

When selecting your emergency fund account, look for these specific characteristics: no monthly fees that would gradually erode your balance, full government deposit insurance protection, no withdrawal penalties or minimum balance requirements that could prevent immediate access in a genuine emergency, and an interest rate meaningfully above the standard market average for savings accounts.

Keeping the account at a different financial institution from your primary checking account adds a small but psychologically valuable layer of friction — the minor inconvenience of a transfer taking one to two business days slightly reduces the temptation to access the funds impulsively for non-emergency purposes.

Step 3 — Start Small and Build Consistently

One of the most psychologically paralyzing aspects of building an emergency fund from scratch is the gap between where you are starting and where you need to eventually arrive. If your target is six months of expenses, perhaps the equivalent of fifteen or twenty thousand dollars or more — and you are starting from zero, the destination can feel so distant that the journey feels pointless before it begins.

The most important reframe for this challenge is this: your first one thousand dollars is the most valuable money you will ever save.

Why the First Milestone Matters Most

Research on financial emergencies consistently shows that a surprisingly large proportion of the financial crises that drive ordinary people into debt are relatively modest in scale — car repairs, medical copays, appliance replacements, home maintenance issues. A fund of even one thousand dollars handles the majority of these common emergencies without any resort to credit or borrowing.

This means that the first one thousand dollars you accumulate does not provide 5 or 10 percent of the protection of a fully funded emergency fund, it provides a dramatically disproportionate share of the practical protection against the most common financial emergencies you are likely to actually encounter. Getting to that first milestone as quickly as possible should be your initial and most urgent priority.

Setting Your Initial Monthly Savings Target

Look at your current monthly budget and identify the most realistic amount you can consistently set aside toward your emergency fund every single month, not the most aspirational amount, but the most realistic one. Even if that amount is twenty dollars, fifty dollars, or one hundred dollars per month, the consistency of the habit matters far more than the size of the initial contribution.

A person who saves fifty dollars per month without interruption will build a more robust emergency fund over time than a person who saves five hundred dollars in a burst of initial enthusiasm and then abandons the habit when life becomes complicated, which it always does.

Set up an automatic transfer from your primary account to your emergency fund account on the same day your income arrives each month, before you begin spending on anything else. This automation removes the emergency fund contribution from the realm of discretionary decision-making and guarantees its consistency regardless of your mood, your competing financial pressures, or the month’s other demands on your attention and resources.

Step 4 — Accelerate Your Progress With Targeted Strategies

While consistent monthly contributions form the foundation of your emergency fund building strategy, several additional approaches can meaningfully accelerate your progress toward your target without requiring any change to your regular income or core expenses.

Direct Windfalls Immediately to Your Emergency Fund

Every time you receive money outside your regular income, a tax refund, a work bonus, a birthday gift, an inheritance, the proceeds from selling unused items, a freelance payment above your usual income — direct some or all of it immediately to your emergency fund before it has any opportunity to be absorbed into general spending.

Windfall money is psychologically different from regular income, because it was not anticipated and factored into your regular budget, its absence is not felt the way a reduction in regular income would be. Directing windfalls to your emergency fund rather than spending them allows you to accelerate your progress dramatically without experiencing any reduction in your regular quality of life.

Conduct a Temporary Expense Audit

Identify two or three discretionary expenses in your current monthly budget that you could reduce or temporarily eliminate for a defined period, three to six months — with the specific, stated purpose of reaching your emergency fund target faster. Knowing that the reduction is temporary and purposeful makes it significantly more psychologically bearable than open-ended sacrifice.

Reducing one streaming subscription, reducing takeaway meals from three times a week to one, or temporarily pausing a non-essential membership for three to six months and directing those savings directly to your emergency fund can meaningfully accelerate your timeline without requiring permanent lifestyle changes.

Generate Additional Income Specifically for the Emergency Fund

Consider whether there are ways to generate modest additional income — selling items you no longer use, taking on occasional freelance work, offering a skill-based service to neighbors or community members — and dedicating the proceeds entirely to your emergency fund. Knowing that the additional income has a specific, defined purpose makes the extra effort feel purposeful and sustainable in a way that general income generation often does not.

Step 5 — Protect, Maintain, and Replenish Your Emergency Fund

Building your emergency fund to its target is a significant and genuinely meaningful financial achievement, but the work does not end there. An emergency fund requires ongoing protection and maintenance to retain its value and its availability when you need it.

Resist the Temptation to Invest Your Emergency Fund

As your emergency fund grows to a substantial balance, you will almost certainly encounter the temptation, or the well-intentioned advice of others, to invest it in something that generates a higher return than a savings account. This temptation should be resisted firmly and completely.

Emergency funds serve a fundamentally different purpose from investment accounts. Their defining characteristic is not growth potential, it is guaranteed, immediate availability. Investments in stocks, bonds, mutual funds, or any other market-linked vehicle involve the risk of loss in value at exactly the moments when you are most likely to need emergency funds, during economic downturns, market crashes, and periods of widespread financial stress that tend to coincide with job losses and other personal financial crises.

The guaranteed availability and capital preservation of a high-yield savings account is not a weakness of emergency fund storage, it is its entire point. Accept the lower return as the cost of the insurance-like protection your emergency fund provides.

Replenish Immediately After Any Withdrawal

When you draw on your emergency fund for a genuine emergency, which is exactly what it is there for — replenishing it as quickly as reasonably possible should become your primary financial priority immediately after the emergency has passed.

A partially depleted emergency fund provides reduced protection against the next emergency, and emergencies have an inconvenient tendency to cluster, a period of personal or economic stress that produces one emergency often produces others in relatively quick succession. Restoring your emergency fund to its full target as promptly as your circumstances allow restores the full protection you have worked to build.

Set up a temporary increase in your automatic monthly emergency fund contribution immediately after any withdrawal, and maintain it until the fund is fully restored to its target balance.

Special Considerations for Different Financial Situations

The universal principle of maintaining an emergency fund applies to virtually everyone, but the specific approach to building and sizing it varies meaningfully depending on your financial situation.

Building an Emergency Fund While Carrying Debt

The question of whether to prioritize emergency fund building or debt repayment is one of the most common and most genuinely difficult personal finance dilemmas. The mathematically optimal answer — pay off high-interest debt first, since the interest rate on debt almost always exceeds the return on savings, conflicts with the practically optimal answer, which recognizes that attempting aggressive debt repayment without any financial buffer typically leads to accumulating more debt every time an unexpected expense arises.

The most widely recommended approach for people carrying significant high-interest debt is a split strategy: build your emergency fund to a minimum threshold, typically one thousand dollars — as quickly as possible, then direct the majority of surplus income toward high-interest debt repayment while maintaining a small ongoing contribution to the emergency fund. Once high-interest debt is eliminated, redirect the full debt repayment amount toward building your emergency fund to its complete three-to-six-month target.

This approach accepts a somewhat longer timeline for both goals in exchange for the financial stability that even a modest emergency fund provides, reducing the likelihood that unexpected expenses will derail your debt repayment progress and force you deeper into the debt cycle.

Building an Emergency Fund on a Low or Variable Income

Building an emergency fund is genuinely more challenging on a low or irregular income — but it is also more urgent, precisely because lower-income households typically have less financial resilience to absorb unexpected expenses and fewer options for borrowing on favorable terms in a crisis.

The key adaptations for low or variable income situations are reducing the initial target to the most achievable meaningful threshold, even three months of minimum essential expenses is transformative compared to zero — and being extraordinarily consistent about making even very small automatic contributions every month without exception.

For freelancers and self-employed individuals with variable monthly income, sizing the emergency fund toward the higher end of the six-month recommendation, or beyond, provides the additional buffer needed to navigate periods of reduced income that are an inherent feature of self-employed financial life.

Common Emergency Fund Mistakes to Avoid

Even financially motivated people consistently make these mistakes when building and maintaining their emergency fund:

- Setting the target too low: A one-month emergency fund is better than nothing but provides inadequate protection against the most consequential emergencies — job loss in particular. Set your target at the three-month minimum from the beginning and work toward six months as your ultimate goal.

- Keeping the fund in an account that is too accessible: Easy access is necessary for genuine emergencies, but instant-transfer availability from the same account you shop with daily is too accessible. A separate account with a slight transfer delay provides the right balance.

- Using the emergency fund for predictable irregular expenses: Annual insurance premiums, car registration, planned medical procedures, and home maintenance are not emergencies — they are predictable expenses that should have their own dedicated savings categories. Raiding your emergency fund for these expenses leaves you unprotected when a genuine emergency arrives.

- Stopping contributions once the target is reached: Inflation gradually erodes the purchasing power of a static emergency fund over time. Review your target annually and increase it to reflect any increases in your essential monthly expenses, ensuring your fund’s real-world purchasing power is maintained.

- Treating the emergency fund as the ceiling of financial ambition: An emergency fund is not the destination of your financial journey, it is the foundation. Once yours is fully funded, the financial habits and automated savings infrastructure you have built in the process of creating it become the platform for pursuing the next level of financial goals, debt elimination, investment, wealth building, and genuine long-term financial freedom.

Conclusion and Final Thoughts

The emergency fund is not the most glamorous personal finance topic. It does not offer the excitement of investment returns, the intellectual complexity of tax optimization, or the aspirational appeal of wealth-building strategies. What it offers instead is something more fundamental and more immediately valuable than any of those things: genuine financial security — the concrete, evidence-based knowledge that when life inevitably delivers its next unexpected blow, you have the resources to absorb it without catastrophic consequences.

My friend whose Tuesday morning phone call launched him into two years of financial stress and recovery eventually built a fully funded emergency fund. He told me recently that the peace of mind it provides, knowing that his family could weather six months of zero income without financial crisis, has changed not just his financial life but his entire psychological relationship with money and with risk.

That transformation is available to everyone who builds this foundation deliberately and maintains it consistently. It does not require a high income, sophisticated financial knowledge, or perfect financial discipline. It requires only the decision to start, the discipline to automate, the patience to build consistently over time, and the wisdom to protect what you have built.

The five steps covered in this guide — determining your target, choosing the right account, starting small and building consistently, accelerating your progress, and protecting and replenishing your fund — give you a complete, practical roadmap to financial resilience that begins with your very next paycheck.

Start today. Start small if you must. But start. Because the most expensive emergency fund in the world is the one you never quite got around to building before the emergency arrived.

How large is your current emergency fund relative to your target, and what has been your biggest challenge in building or maintaining it? Share your honest experience in the comments below. Whether you are just starting from zero or celebrating a fully funded fund, your story could be the motivation another reader needs to finally take this most important financial step.

{kind=link}