For most of my twenties, the word “budget” triggered an immediate and visceral reaction somewhere between boredom and dread. I associated it with spreadsheets I would never finish building, sacrifices I was not willing to make, and a level of financial discipline that seemed reserved for people who were somehow fundamentally more organized and self-controlled than I was. So I did what most people do, I ignored it entirely, spent more or less whatever came in each month, told myself I would start being more careful “next month,” and wondered every January why my financial situation looked exactly the same as it had the January before.

The shift came when a financially savvy colleague introduced me to a concept so elegantly simple that I genuinely could not believe it had taken me this long to encounter it. It was not a complex investment strategy or a sophisticated financial planning system. It was three numbers: 50, 30, and 20.

The 50/30/20 rule is a budgeting framework so straightforward that it can be explained in a single sentence, so flexible that it works for almost any income level, and so psychologically intelligent that it removes the guilt and deprivation that make most budgeting attempts fail within the first two weeks. It does not ask you to track every coffee purchase or deny yourself every small pleasure. It simply asks you to divide your income into three broad, meaningful categories — and then live intentionally within each one.

In this guide, you will learn exactly what the 50/30/20 rule is, where it came from, how to apply it to your specific income and expenses in practical step-by-step terms, how to customize it when your financial situation demands flexibility, and the specific habits and tools that will make it stick as a long-term financial practice rather than another abandoned good intention.

Whether you are living paycheck to paycheck and trying to find a way out, earning a comfortable income but somehow never getting ahead, or simply trying to build the financial foundation for a more secure and free future, the 50/30/20 rule gives you a framework that actually works, because it is built around real human psychology rather than theoretical financial perfection.

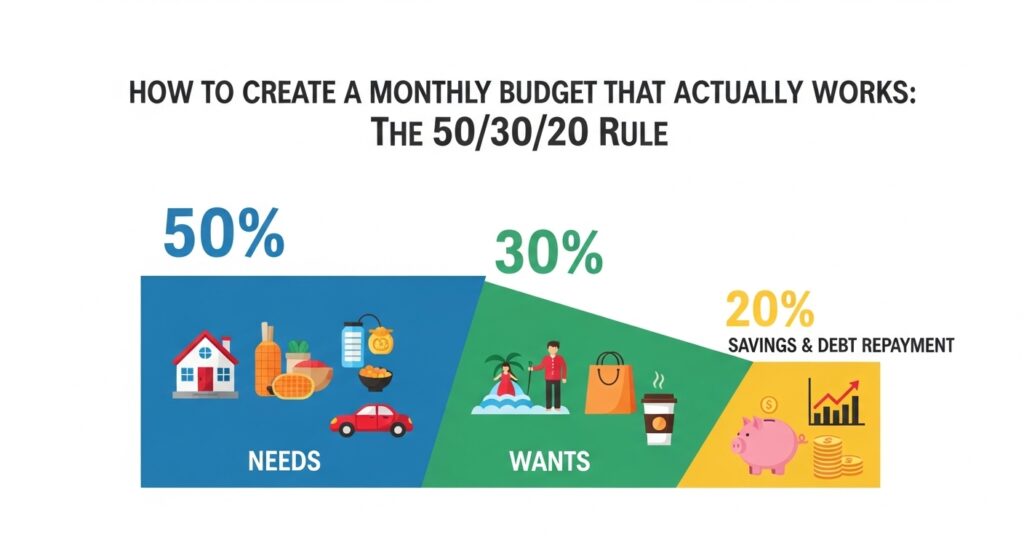

What Is the 50/30/20 Rule and Where Did It Come From?

The 50/30/20 rule was popularized by US Senator Elizabeth Warren and her daughter Amelia Warren Tyagi in their 2005 book All Your Worth: The Ultimate Lifetime Money Plan. Warren, a Harvard Law professor and bankruptcy expert at the time, had spent years studying the financial lives of ordinary American families and trying to understand why so many people, including many with decent incomes — consistently found themselves in financial crisis.

Her research led her to conclude that most budgeting advice fails not because people lack discipline, but because it is overcomplicated, overly restrictive, and fundamentally misaligned with how human beings actually think and feel about money.

The 50/30/20 framework was her answer, a simple, psychologically realistic structure that balances financial responsibility with genuine quality of life.

The core principle is straightforward: after calculating your after-tax monthly income, you allocate your spending across three broad categories using a percentage split. 50 percent goes toward your needs — the essential expenses that are non-negotiable for basic living. 30 percent goes toward your wants — the lifestyle choices that make life enjoyable and meaningful beyond bare necessity. 20 percent goes toward your financial goals — savings, debt repayment, investments, and emergency funds that build your financial security and future freedom.

That is the entire framework. Three categories. Three percentages. One monthly conversation with your money that, practiced consistently, can permanently transform your financial trajectory.

Step 1 — Calculate Your True Monthly After-Tax Income

Before you can apply the 50/30/20 rule, you need one essential piece of information: your actual monthly take-home income — not your gross salary, but the real amount that lands in your bank account after taxes, pension contributions, health insurance premiums, and any other deductions are removed.

For Salaried Employees

If you receive a regular monthly salary, your after-tax income is simply the amount deposited into your bank account each pay cycle. Check your most recent pay stub or bank statement to confirm the exact figure. If you are paid bi-weekly rather than monthly, multiply your bi-weekly take-home pay by 26 and divide by 12 to arrive at your average monthly after-tax income.

For Freelancers and Self-Employed Individuals

Calculating after-tax income is somewhat more complex for freelancers and self-employed individuals because income tends to vary month to month and tax obligations must be set aside manually rather than deducted automatically by an employer.

The most practical approach for freelancers is to calculate your average monthly income over the past six to twelve months, then subtract your estimated tax liability, typically between 25 and 35 percent of gross income depending on your location and business structure, to arrive at a conservative estimate of your monthly after-tax income. It is always smarter to budget based on a slightly conservative income estimate and be pleasantly surprised by a surplus than to budget based on an optimistic figure and consistently fall short.

If your income varies significantly month to month, consider basing your budget on your lowest typical monthly income rather than your average. This approach ensures that your essential needs are always covered even in slower months, while surplus income in stronger months can be directed entirely toward your financial goals.

Including All Income Sources

Remember to include all legitimate sources of monthly income in your calculation — not just your primary salary or freelance earnings. Side income, rental income, consistent investment dividends, and any other regular income streams should all be factored into your total monthly after-tax figure.

Step 2 — Understand and Calculate Your Needs (The 50 Percent Category)

The first and largest category in the 50/30/20 framework covers your needs — the essential expenses that you genuinely cannot avoid without significant disruption to your basic standard of living.

What Counts as a Need

Needs are the non-negotiable expenses that must be paid regardless of your preferences or financial goals. They typically include housing costs such as rent or mortgage payments, utility bills including electricity, water, and internet access, essential groceries and food, basic transportation costs including car payments, fuel, or public transit, minimum debt repayments on existing loans, essential insurance premiums, and any non-negotiable medical expenses.

The critical distinction here, and one that many people get wrong when first applying this framework, is between genuine needs and habitual expenses that feel like needs. Your monthly rent is a need. A premium apartment that costs twice what adequate housing in your city would require is partially a want. Basic grocery spending is a need. Weekly grocery deliveries with premium add-ons may be partially a want. Understanding and honestly making this distinction is one of the most valuable financial clarity exercises the 50/30/20 rule prompts you to undertake.

What to Do If Your Needs Exceed 50 Percent

This is the question most people ask first, and the answer is important. If your essential expenses currently exceed 50 percent of your after-tax income, which is the reality for many people living in high-cost cities or carrying significant debt, the 50/30/20 rule does not fail you. It diagnoses you.

When your needs category is eating more than half your income, it reveals a structural imbalance in your financial life that temporary spending cuts in your wants category cannot sustainably fix. The real solution requires addressing the underlying structural issue, finding ways to reduce major fixed costs like housing or transportation, increasing your income through additional work or career advancement, or aggressively paying down high-interest debt that is consuming a disproportionate share of your monthly income.

In the meantime, adjust your percentages temporarily, perhaps 60/20/20 or 65/15/20 — while actively working to bring your needs category back toward the 50 percent target over time. The framework is a guide, not a rigid rule that fails if your first calculation does not fit perfectly.

Step 3 — Define and Protect Your Wants (The 30 Percent Category)

The 30 percent wants category is what makes the 50/30/20 rule psychologically sustainable in a way that most other budgeting frameworks are not.

Most traditional budget advice treats every non-essential expense as a financial sin to be eliminated, cut the daily coffee, cancel the streaming subscriptions, never eat at a restaurant, deny yourself every small pleasure in the name of financial responsibility. This approach works brilliantly in theory and collapses almost immediately in practice, because human beings are not wired to sustain prolonged deprivation cheerfully.

The 50/30/20 rule takes a fundamentally different and far more realistic approach. It acknowledges that a life with no enjoyment, no leisure, no social activities, and no small pleasures is not a life most people can or should sustain indefinitely, and that a budget which allows for genuine quality of life is far more likely to be maintained long-term than one built entirely around sacrifice.

What Counts as a Want

Wants are the lifestyle expenses that go beyond bare necessity and contribute to your enjoyment, comfort, social life, and personal fulfillment. They include dining out and takeaway meals, entertainment subscriptions like Netflix, Spotify, and gaming platforms, gym memberships and fitness classes, clothing beyond basic necessities, travel and vacations, hobbies and leisure activities, personal care beyond essentials, and the premium versions of things you could have more cheaply if you chose to.

Spending Your 30 Percent Intentionally

The wants category is not a license to spend 30 percent of your income on whatever impulse strikes first. It is an invitation to spend that portion of your income on the things that genuinely bring you the most joy, satisfaction, and meaning, which requires actually thinking about what those things are rather than letting spending happen on autopilot.

A powerful exercise within the wants category is to review three months of your discretionary spending and honestly assess which expenses genuinely enriched your life and which ones you spent without much thought and barely remember. Redirect the budget previously consumed by low-value habitual spending toward the experiences and choices that actually matter to you. This process — sometimes called intentional spending — transforms the wants category from a source of guilt into a genuinely enjoyable aspect of your financial life.

Step 4 — Maximize Your Financial Goals (The 20 Percent Category)

The 20 percent financial goals category is the engine of long-term financial transformation — the portion of your monthly income that, invested consistently over time, has the power to completely change the trajectory of your financial future.

The Three Priorities Within the 20 Percent Category

Not all financial goals are equally urgent, and the order in which you fund them matters significantly.

The first priority within your 20 percent is building a emergency fund — a liquid cash reserve held in an accessible savings account containing three to six months of your essential living expenses. An emergency fund is the financial foundation that prevents a single unexpected event — a medical bill, a car repair, a period of unemployment — from derailing your entire financial plan and forcing you into debt. Until you have this safety net in place, it should receive the majority of your 20 percent allocation every month.

The second priority is high-interest debt repayment — aggressively paying down credit card balances, personal loans, and any other debt carrying an interest rate significantly above what you could reasonably earn through saving or investing. Paying off a credit card charging 20 percent annual interest is the financial equivalent of earning a guaranteed 20 percent return on your money — an opportunity that no investment in the world can reliably match.

The third priority, once your emergency fund is established and high-interest debt is under control, is long-term savings and investment — contributing to a retirement account, building an investment portfolio, saving toward a specific major financial goal like a home purchase, or building additional financial security for your future self. The power of compound interest — earning returns not just on your initial savings but on the accumulated returns from previous periods — means that money invested consistently from a relatively young age grows to amounts that can seem almost magical over a twenty or thirty-year horizon.

Automating Your 20 Percent

The single most effective strategy for ensuring your financial goals category actually receives its intended allocation every month is automation. Set up an automatic transfer from your primary bank account to a dedicated savings or investment account on the same day your income arrives each month — before you have any opportunity to spend that money on other things.

This principle — often called paying yourself first — removes the financial goals contribution from the realm of discretionary decision-making and makes it as automatic and non-negotiable as paying your rent. When the transfer happens automatically before you begin spending, you never experience the money as available for other purposes, which eliminates the temptation to redirect it when your wants feel more pressing than your future financial security.

Step 5 — Track, Review, and Adjust Your Budget Monthly

Creating a 50/30/20 budget is not a one-time event — it is the beginning of a monthly financial practice that becomes more effective, more intuitive, and more powerful the longer you maintain it.

Choosing Your Tracking Method

The best budgeting tracking method is whichever one you will actually use consistently. For some people that is a detailed spreadsheet. For others it is a dedicated budgeting app. For minimalists it might be as simple as a monthly check-in with their bank statement and three labeled columns in a notebook.

Budgeting apps like YNAB (You Need A Budget), Mint, and PocketGuard can dramatically simplify the tracking process by automatically categorizing your transactions and showing you in real time how your spending in each category compares to your budgeted allocation. Many of these tools send alerts when you are approaching the limit in a particular category — providing a timely nudge to course-correct before you overspend rather than a painful realization at the end of the month.

For those who prefer a more hands-on approach, a simple budgeting spreadsheet with columns for your three categories, your budgeted amounts, your actual spending, and the variance between the two provides all the information you need to manage your budget effectively. Microsoft Excel and Google Sheets both offer free budgeting templates that can be customized to match the 50/30/20 structure in minutes.

The Monthly Budget Review

Set aside thirty minutes at the end of each month — the same time, the same day, every month — to review your actual spending against your budgeted allocations in each of the three categories.

This monthly review is not an exercise in self-criticism. It is a data collection and decision-making session. Which category ran over budget and why? Was it a genuine one-time anomaly or a recurring pattern that suggests your budget allocations need adjustment? Which category came in under budget, and where should that surplus be redirected? What financial goals did you make progress on this month, and what would accelerate that progress next month?

Over time, this monthly review process builds a level of financial self-awareness and intentionality that progressively improves every aspect of your financial life — not just your adherence to the 50/30/20 framework, but your relationship with money as a whole.

How to Customize the 50/30/20 Rule for Your Specific Situation

One of the most important things to understand about the 50/30/20 rule is that the percentages are a starting framework and a target to work toward, not a rigid prescription that must be followed precisely regardless of your individual circumstances.

Adjusting for a High Cost-of-Living Area

If you live in a city where housing costs alone consume close to 40 or 50 percent of a typical income — which is the reality in many major metropolitan areas around the world in 2026 — a strict 50/30/20 split may not be immediately achievable. In this situation, consider a modified split such as 60/20/20 or 65/15/20 while actively pursuing strategies to reduce your housing costs over time — whether through finding a more affordable living situation, seeking income growth, or both.

Adjusting for Aggressive Debt Repayment Goals

If you are carrying significant high-interest debt and want to eliminate it as quickly as possible, consider temporarily redirecting a portion of your wants allocation to your financial goals category — perhaps a 50/20/30 split where 30 percent goes toward debt elimination and savings until the debt is cleared. Once the debt is gone, redirect that allocation back to the wants category and experience the significant improvement in quality of life that debt freedom makes possible.

Adjusting for Early Retirement or Aggressive Savings Goals

If financial independence or early retirement is a specific goal you are working toward, you may choose to significantly increase your financial goals percentage — perhaps to 30, 40, or even 50 percent — by making deliberate, chosen reductions in your wants category. The key word is chosen — this level of savings intensity is sustainable only when it is a conscious decision aligned with deeply held values and goals, rather than a sacrifice imposed from the outside.

Common Budgeting Mistakes the 50/30/20 Rule Helps You Avoid

Understanding the pitfalls that derail most budgeting attempts helps explain why the 50/30/20 framework is so much more effective than traditional line-item budgeting for most people:

- Tracking every penny instead of every category: Line-item budgeting — where you set and track a specific spending limit for every individual expense — creates so much administrative complexity that most people abandon it within weeks. The 50/30/20 rule replaces this with three broad categories that are easy to monitor and maintain without obsessive detail tracking.

- Treating all debt payments the same way: Minimum payments on debt are a need — they must be made. Extra payments above the minimum are a financial goal — they build your future. Understanding this distinction helps you correctly categorize debt payments and recognize the difference between servicing debt and eliminating it.

- Ignoring irregular annual expenses: Annual insurance premiums, car registration fees, subscription renewals, and other expenses that do not occur monthly can completely derail a monthly budget if they are not planned for. Divide all your annual irregular expenses by twelve and include that monthly equivalent in your needs category planning every month, setting the money aside in a dedicated savings buffer so it is available when the bill arrives.

- Giving up after one bad month: Every person who has ever maintained a successful long-term budget has had months where the plan fell apart — unexpected expenses, income disruptions, or simply a loss of discipline for a few weeks. The response to a bad month should never be abandonment. It should be a calm assessment of what happened, a reset of the allocations for next month, and a recommitment to the framework. Consistency over time, not perfection in any single month, is what produces lasting financial transformation.

- Not celebrating financial milestones: Building an emergency fund, paying off a credit card, reaching a savings target — these are genuine achievements that deserve genuine acknowledgment. Building small celebrations into your financial journey maintains the motivation and positive emotional association with your budget that makes it sustainable for the long term.

The Tools That Make the 50/30/20 Rule Easier to Maintain

Beyond the budgeting apps mentioned earlier, a few additional tools and practices can significantly enhance the effectiveness and sustainability of your 50/30/20 budget:

A dedicated savings account for each financial goal — rather than keeping all your savings in a single account, makes it dramatically easier to track progress toward specific goals and psychologically harder to dip into savings for non-emergency purposes. Most modern banks and digital banking platforms allow you to open multiple named savings accounts at no cost.

A separate spending account for your wants category — funded at the beginning of each month with your 30 percent wants allocation, creates a natural, automatic spending limit for discretionary expenses without requiring constant mental arithmetic. When the wants account is empty, discretionary spending for the month is done. This simple structural trick eliminates the need for willpower in managing your wants spending.

Weekly five-minute financial check-ins — a brief, regular glance at your spending in each category to ensure you are on track, prevent the monthly review from revealing large, unpleasant surprises. Small course corrections made weekly are far less painful than large corrections required when a category has significantly overrun by month-end.

(For guidance on keeping your financial accounts and personal data secure while managing your money online, check out our guide on [How to Secure Your Personal Data: 7 Essential Cybersecurity Tips for 2026].)

Conclusion and Final Thoughts

The 50/30/20 rule works not because it is mathematically sophisticated or financially complex — it is neither. It works because it is built around a deeply honest understanding of human psychology and the real reasons most budgeting attempts fail.

It works because it gives you permission to enjoy your money, not just guard it. It works because it replaces the paralyzing complexity of tracking hundreds of individual expenses with three clear, memorable categories that anyone can manage. It works because it connects your daily spending decisions to your long-term financial goals in a way that makes every choice feel meaningful rather than arbitrary. And it works because it is flexible enough to accommodate the messy, unpredictable reality of actual financial life rather than demanding the impossible perfection that makes most budgets collapse.

The three numbers — 50, 30, and 20 — represent something far more significant than a budgeting formula. They represent a philosophy of financial life that balances security with enjoyment, discipline with flexibility, present satisfaction with future freedom.

My financial life looks unrecognizably different today from those early years of willful ignorance and monthly financial drift. Not because my income dramatically changed overnight, but because I finally started having an intentional, honest monthly conversation with my money, and the 50/30/20 rule gave me the framework to have it.

That same conversation is available to you. It starts this month. It starts with three numbers and a willingness to look honestly at where your money is going and where you want it to take you.

Are you going to try the 50/30/20 rule this month, and which of the three categories do you think will be the biggest challenge for you to get right? Share your thoughts in the comments below. Whether you are just starting your budgeting journey or looking to refine a system you already have, your experience could be exactly the encouragement another reader needs to finally take control of their financial life.

{kind=link}